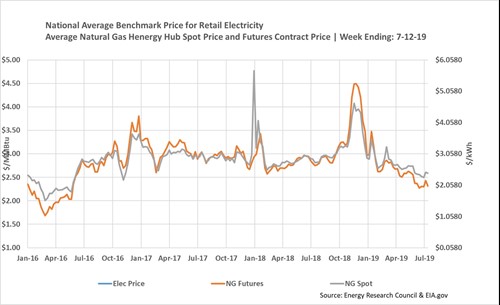

Retail electricity prices are largely driven by natural gas prices. Even though power is generated from a variety of sources—hydroelectric, wind, solar, nuclear, coal, gas— generating plants are paid based on the last fuel used to meet demand, which is almost always natural gas. Therefore, the amount you pay per kWh for electricity is determined primarily by the current price of natural gas in your region.

Natural gas prices are constantly fluctuating based on a balance between supply and demand. Demand is driven by electricity generation (power burn), commercial & industrial usage, and exports to Mexico or oversea in the form of liquid natural gas. Supply is generally a function of domestic gas production and Canadian gas imports.

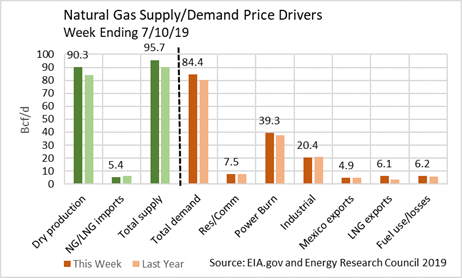

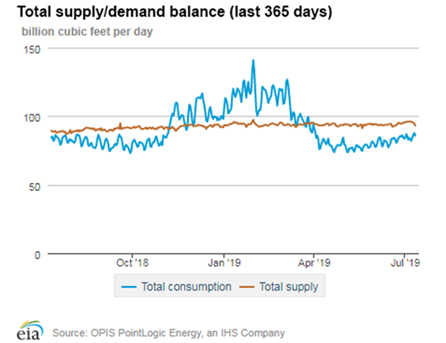

If natural gas production is expected to exceed demand, natural gas prices (and therefore power prices) are pressured downward. If demand looks like it will grow faster than natural gas production, prices trend upward. The basic scorecard the market uses to assess natural gas supply/demand is summarized in the accompanying graphs. Natural gas production has exceeded demand since the end of last winter. This has pressured natural gas prices downward to historic lows, reaching $2.16/MMBtu in late June. Since then, however, natural gas prices have begun to edge upward, ending last week (7/12/19) around $2.44/MMBtu.

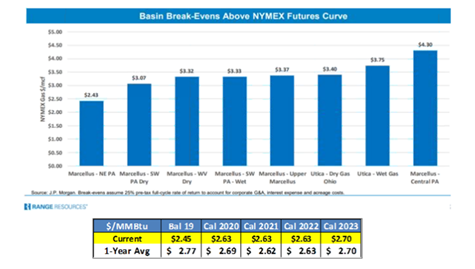

The main reason Is that natural gas prices have dropped below the cost of production. Individual well break-even rates vary by region, but general proxy rates pivot around $2.50/MMBtu before considering average costs and corporate overhead.

Consequently, production has flattened and even declined. Producers are facing increasing pressure from investors to show financial discipline and generate a positive rate of return. See WSJ article from 6/7/19 “Frackers Scrounge for Cash as Wall Street Closes Doors.” In the prolific Marcellus/Utica NE shale gas basin the Drilled-But-Uncompleted wells (DUC) inventory that producers tap to generate new production has been depleted. New well drilling permit applications have dropped by over 50% since the start of this year and production levels are beginning to drop off quickly.

In the Permian Basin, which together with Marcellus/Utica accounts for almost half of all domestic production, most of the production wells have been brought online over the past year to take advantage of high oil prices. Over 30% of NG production comes as a biproduct from oil drilling. But approximately 70% of a new well’s productivity is exhausted in the first year of operation. That means that most of the producing wells in the Permian will likely slow considerably as time moves forward.

Less capital investment plus lower DUC inventories equal a big drop in Appalachian wells coming online in 2019. Fewer wells mean a lower rate of production. In the Permian basin, investors will likely limit addition capital investment for drilling new wells and the current inventory will likely begin to slow as the majority moves into their second year of production. Anything less than blistering production growth is likely to pressure natural gas (and power) prices upward. With demand continuing to escalate due to surging U.S LNG export capacity, pipeline exports to Mexico and gas-fired power demand for domestic use, natural gas (and therefore power) prices are likely to begin moving northward.