Entering the winter, our projections called for a long, cold season that put a strain on the already historically low natural gas storage levels. What we’ve so far experienced is a volatile, hard-to-predict winter with temperatures oscillating between unseasonable highs to bursts of cold. We discussed polar vortices in an article last year. It’s a term that is often incorrectly cited as an uncommon or unusual event by members of the media, as happened often in the cold 2013-2014 North American winter.

In actuality, the polar vortices are persistent atmospheric zones, rotating around the Earth’s poles and condensing arctic air. When the vortex is strong, the air is contained and we in the United States are typically not affected by sharp, cold arctic winds. When it is very weak, the air becomes disorganized and is pushed out towards the equator, creating sudden and severe drops in temperature. These weak polar vortices create the event that many people think of as “the polar vortex” – an anomalous severe temperature drop caused by the southward shift of the weak northern polar vortex.

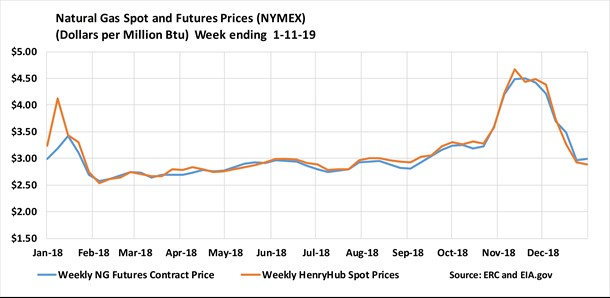

Currently, natural gas prices prove increasingly volatile. After seeing significant gains in November (in anticipation of the pricing pressure caused by low storage levels), prices plummeted back down to rest around or below the $3/MMBtu point during December. Prices picked up during mid-January as a nor’easter caused massive snowstorms across the Eastern U.S. in what could be classified as an event related to a weak northern polar vortex.

In the Algonquin Citygate, which serves Boston, prices fluctuated wildly between $11.38/MMBtu to $3.53/MMBtu week-over-week. Henry Hub, often seen as an indicator of market health for natural gas, dropped from $3.61 to $3.10/MMBtu during that same week.

Looking aside from weather, new industrial plants are being developed in the United States. This is expected to increase consumption of natural gas, which has been growing steadily since 2009. Favorable natural gas prices, because of the shale revolution, have led to industries that use natural gas for chemical production, Methanol, ammonia, and fertilizer. These industries are heavy users, requiring natural gas for both feedstock and heating (as natural gas is the most popular heating source in the United States). The EIA forecasts that these products will drive growth in demand through 2020. It forecasts 23.2 Bcf/d for industrial consumption in 2019, 2% higher than 2018’s levels.

Production saw a rare decrease at time of writing, falling 1% week-over-week. This may be in large part due to declining rig count, another rarity in the modern day. Week-over-week, natural gas rig count decreased by 4 to 198, and oil-directed rigs fell by 21 to 852. While natural gas production can continue high even as natural gas rigs decline, it is the associated loss of oil rigs (which can produce natural gas as a by-product) that likely caused the overall fall in production. This represents the largest decrease in week-over-week rig count since February of 2016.

This volatile market creates interesting conditions for U.S. consumers. In terms of short-term pricing, the volatility in the market could make for very favorable or very unfavorable prices depending on timing. Locking in while the market is low could result in a favorable contact over the next few years, whereas mistiming the market may lock a consumer in an unfavorable contract. Market-based prices are strongly discouraged, as the volatility would lead to budget uncertainty and likely increased expenses.

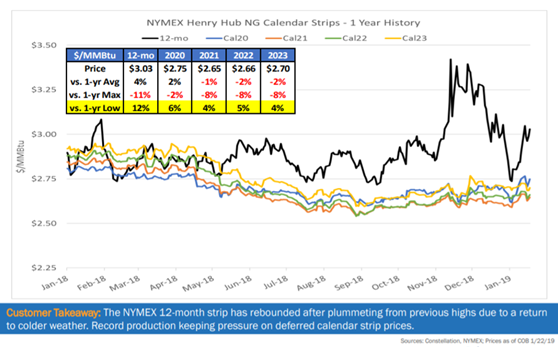

In terms of long-term pricing, this may be an excellent time to begin considering renewal for a contract beginning a year or more in the future. When near-term market conditions result in unstable and volatile pricing, future contract terms become discounted by comparison. This is called “backwardation” and occurs because the market is recognizing that anomalous short-term factors are unlikely to be present during winters 1-3 years in the future. For example, the industry expects that 7.5 gigawatts of natural gas-powered electricity will come online by the end of 2019. 1 gigawatt can power roughly 700,000 homes, as a point of reference. The market anticipates this increased capacity, and as such futures contracts are deeply discounted compared to the short term 12-month term.

Looking ahead, much will depend in large part on what happens with winter weather. Half of the winter season is in the history books, so it would take a sustained cold for prices to significantly rally again. However, that’s precisely what we saw last year; it was not simply the frequent snowstorms of the 2017-18 winter season that drove storage levels so low, but the fact that these cold temperatures lingered into April. In short, the 12-month strips reflect intense weather based-volatility, whereas future strips are reflecting favorable and stable prices due to the forces of backwardation.

APPI Energy monitors the market, ensuring we stay informed about all current events that may affect electricity and natural gas prices. Utilizing years of historic data, we provide our customers with data-driven recommendations designed to help save time and create budget certainty during the energy procurement process. For more information about market conditions, and how APPI Energy can help your organization stay ahead of energy prices, please call us at 800-520-6685 or contact us via our website.