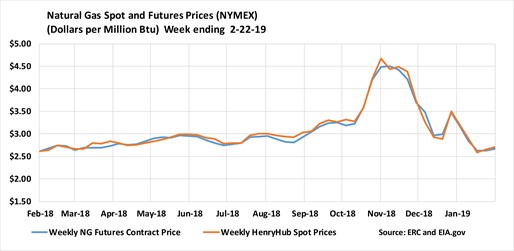

In 2018, we saw a natural gas market emerge from the winter demand season in a volatile state. Despite record production, an extended cold front throughout March and April of 2018 across the major demand centers of the United States caused a historically late beginning to the spring replenishment season, with the first injection into storage taking place in the third week of April. With the withdrawal season ending so late, concern grew about the gap of natural gas storage levels compared to the five-year average. There was a 30% difference between storage levels at the end of Winter ’18 and the five-year average at the time, however strong injections throughout June lowered the deficit to 19.5% by early summer.

These circumstances gave way to the state of the natural gas market we are seeing in 2019. While natural gas injections remained strong leading up to the winter 2019 withdrawal season, storage levels were at a deficit of 20% to the five-year average at the beginning of winter, and weather forecasts predicted that we would see another cold winter much like that of 2018. Weather, as it turns out, is perhaps the most defining factor of the natural gas market, especially as it relates to 2019. In this article, we will examine the supply and demand factors that affect the natural gas market of today and analyze how current events are likely to affect power prices going forward.

Supply Factors

The general supply-side factors affecting natural gas prices are typically identified as production, imports, and storage levels. While production and imports directly impact the supply of natural gas, storage levels serve as an indicator of our supply of natural gas versus current market demand. It is, by law, publicly reported on a weekly basis to the Energy Information Administration (EIA), and often influences natural gas prices.

Storage

We entered the winter of 2019 with storage levels in deficit of 30% to the five-year average, normally a sign that prices are likely to trend upward, especially with predictions of a cold winter. However, early winter forecasts proved misguided. Despite a few polar-vortex related weather events, January of 2019 was marked as the 3rd warmest on record since these highs and lows started being tracked 140 years ago. There were some cold fronts in December, which kept natural gas storage levels at 20% lower than the five-year average, but these deficits shifted to 11% during the warm January. Going forward, we will have to see how March and April trend to fully realize the effects of storage on the market. If, like last year, we see extended colds and a delayed start to the injection season, prices will likely trend upwards.

Production

Despite low storage levels, which typically increase natural gas prices, production continued to serve as a hard cap on frequent or sustained price growth for the natural gas market. We’ve experienced some sharp demand spikes this winter, but the spikes in pricing were short-lived and isolated. This is in large part due to continually high production bolstering and helping to cushion sudden and dramatic increases to demand. Natural gas production has trended increasingly high due in large part to more efficient drilling operations and increased oil prices present during late 2018 and early 2019. Natural gas production as a byproduct of oil drilling is a huge factor when it comes to the production of natural gas, even as natural gas specific rig counts may flatten or even decline.

Imports

Despite our abundance of natural gas production, we rely on Canadian natural gas imports to supply parts of the country that are not serviced by pipeline networks and do not have the capacity to utilize U.S. produced gas for power generation and heating demand. Canadian gas is imported primarily to satisfy the needs of the western and midwestern U.S., so prices in these areas are typically affected by domestic Canadian demand as well as their own heating needs.

Natural gas imports into the United States have been declining since 2007, due in large part to ramping U.S. natural gas production. The U.S. became a net exporter for natural gas in 2017.

Demand Factors

The demand factors for natural gas can be summarized as weather, economic growth, exports, and the availability and prices of competing fuels. The first of these factors is perhaps the most defining thus far in 2019. Weather is never fully predictable, simply because nature’s volatility and environmental factors render well-informed and reasonable analysis fallible.

Weather

As mentioned, the winter weather of 2018 set the stage for the ’19 season. Cold fronts through April 2018 caused a late start to the injection season, and despite promising injections through the following summer, we entered winter of ’19 at a storage deficit. Predictions were, at the time, that winter would prove long and cold. However, January of 2019 was the third warmest on record. Interestingly, the reverse also proved true. When winter forecasts projected a warm February, the United States was hit with a polar vortex-related weather event that caused immense heating-related energy demand and spiked prices temporarily in some communities.

Going forward, we should continue to expect anomalous and unpredictable weather to be a factor in our estimates of energy. Historical data shows that weather anomalies are increasing in frequency throughout the latter half of this decade, and we have not yet seen indication that temperatures will begin to follow a pattern of historic norms again in the years to come.

Economic Growth

Economic growth is a major factor in the natural gas market for a simple reason: businesses need power. There are conflicting opinions over the measurement of manufacturing growth, but factually speaking, the growth of manufacturing in the United States is growing faster than overall GDP which is a sign that we are seeing some increases in the industry domestically.

One particular sector that is expected to generate increased natural gas demand is in methanol plants. Methanol plants are among the most natural gas-intensive industrial users, as they require the gas both as a feedstock and to process heat. EIA reports that three new plants are expected to come online this year and in 2020, which will add significantly to the consumption of natural gas domestically. One plant, expected to be the largest in the country, is estimated to consume 0.15 billion cubic feet per day.

Exports

Substantial growth has been seen in the field of Liquefied Natural Gas or LNG exports. In addition to our growing exports to Mexico, the U.S. has found an attractive market in the transport of LNG from export terminals to countries across the ocean. Recently, FERC worked through a gridlock to approve a new LNG export terminal for the first time in two years. This new export terminal is a major step towards EIA’s projection that the U.S. will launch an additional 3 export terminals and more than double its current LNG export capacity to 8.9 Bcf/d by the end of this year.

As LNG export capacity increases, there will be more incentive for companies to transport their LNG to places such as Asia and Europe that wish to transition away from less-efficient and more pollutant coal-fired power plants to natural gas. By the same token, that means that the supply of domestic natural gas shall decrease, which is a bullish factor for natural gas prices.

Competing Fuels

Natural gas production began in earnest in the United States during 2007. Not coincidentally, coal consumption peaked that same year, and has been on a decline ever since. April of 2015 was the first year that more electricity was generated from natural gas than from coal on a monthly basis, 2016 the first year-over-year annual basis. 2017 and 2018 have continued that trend, and in the U.S. today it is apparent that natural gas will continue to increase as coal consumption declines. The primary reason for this is the cost of coal comparatively to natural gas. Natural gas prices have remained relatively low since the growth of gas in 2007, and this sustained low price has kept the cost of generating electricity with the resource more competitive than that of coal.

Environmental concerns have also played a large factor in the growth of natural gas demand as comparable to coal. The 2015 requirement of the Mercury and Air Toxics Standards represented a peak in coal-fired electric generator retirements, partially due to age, but also due to an inability of the plants to meet the standards. Retirements have continued throughout the years since; 2018 saw many coal plants retire. Natural gas, on the other hand, has far fewer emissions than coal which has helped sustain its growth.

Moving into 2019, it will be interesting to see what comes of renewables and their relationship to natural gas related demand. Congress has signaled some interest in pursuing a push towards more renewable energy sources, but we will have to see if and how that manifests before determining its exact impact as related to natural gas as a market.

The Future

As we look toward the future, we should likely expect weather-related volatility, environmental impact, and economic factors to play a major role in both natural gas and the energy market as a whole. These factors have begun to make their way into the national discourse, which is often an indication of the market’s trend. What exactly comes of the national discourse is unknown, but it will be interesting to monitor how the market reacts to the modern landscape.

For more information and insight into energy market trends, as well as trusted consulting-based solutions for energy supply procurement, please visit APPI Energy at www.appienergy.com or call APPI Energy at 800-520-6685. For 23 years, APPI Energy has delivered apples-to-apples comparisons of supplier prices and contracts and negotiates supply solutions that reduce and manage energy costs on an ongoing basis for commercial and industrial customers.